13 min

4

04.08.2025

.jpeg)

For many students, earning a college degree comes with a shadow that lingers long after graduation—years of debt that shape their financial future. The cost of attending college can be extremely high, as students have to pay for everything from tuition to room and board and other expenses. The costs for books, transportation, and other assets can also add up after a while. These expenses make it so that students have to take out loans to cover their college expenses.

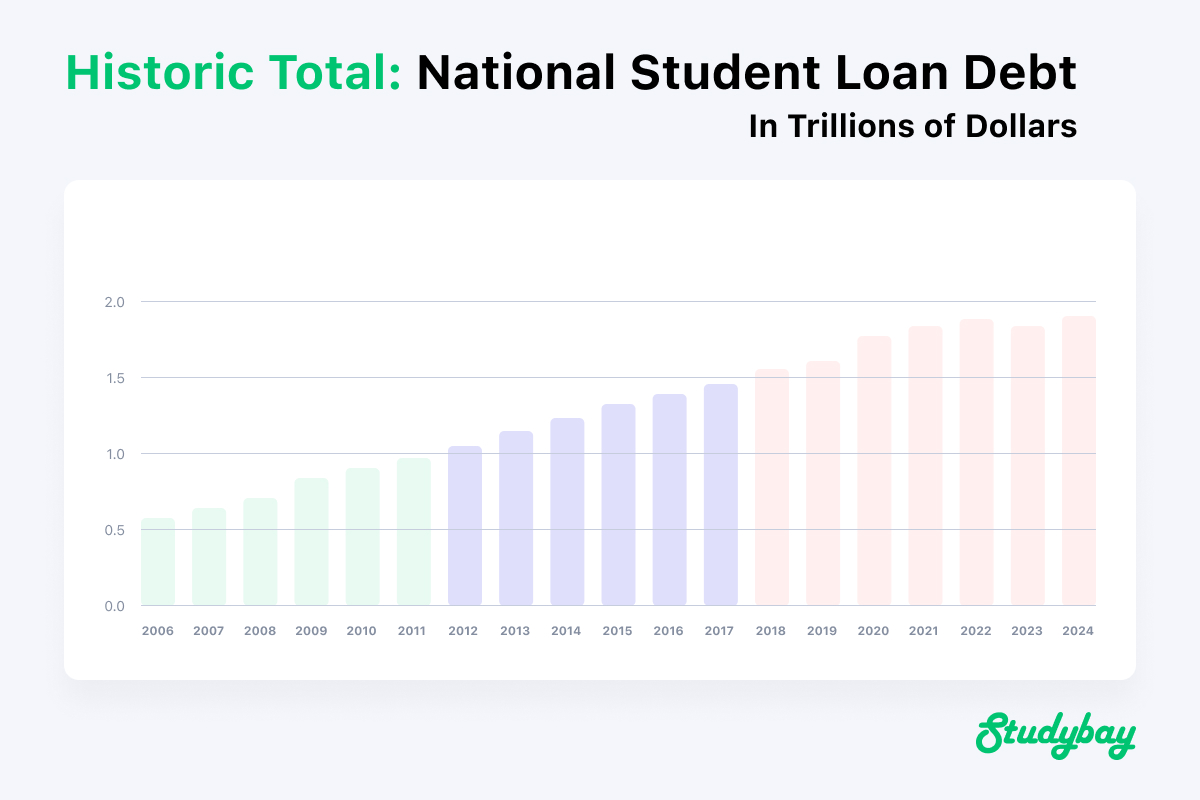

Student loans have been necessary for many people, but the expenses of those loans continue to add up long after graduation. According to the Education Data Initiative, Americans have about $1.77 trillion in student loan debts as of the fourth quarter of 2024. It’s estimated that about 42.7 million borrowers have federal loan debt, meaning students who have debt owe about $40,000 on average.

The Education Data Initiative also reports that the timeline to pay off student debt can be extensive. It has been calculated that it takes about 20 years on average to repay student loan debt, and fewer than half of borrowers are on a basic 10-year plan that includes fixed payments.

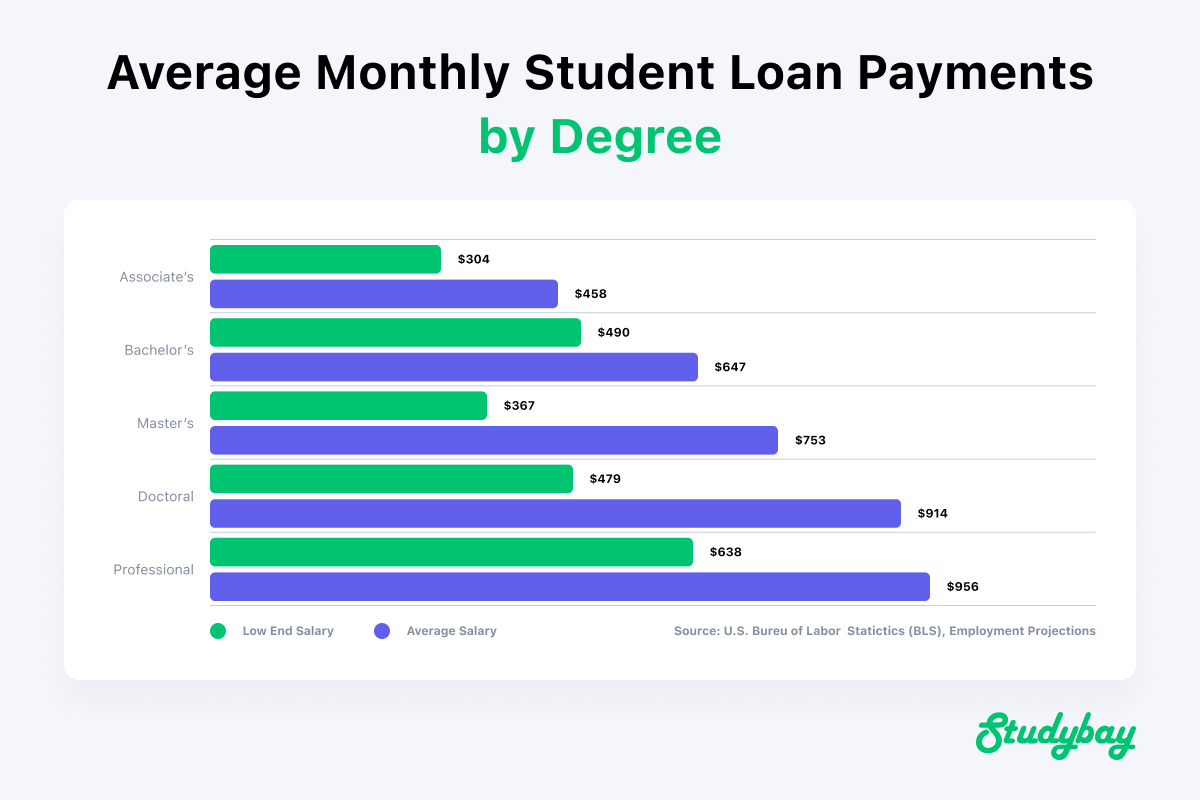

The general monthly student loan payment is also very high, as students spend about $500 monthly to pay off debt. This is higher on average when a person has a more valuable degree.

These totals show that alumni are spending more money on their education than ever before, and they’re paying for it decades after graduation. Such expenses are making it tougher for alumni to manage their lives, as they don’t have as much money to help them manage other expenses or plan future events.

Paying Well After College

To understand the concern of student loan debt, it helps to see how long it takes for someone to pay off a loan. The U.S. Department of Education’s Federal Student Aid website states that repayment plans for student loans can go from 10 to 30 years on average. Those who don’t enter any repayment plans will automatically enter setups where they pay at least $50 a month with interest adding up on whatever one owes.

A standard loan can last up to ten years, while direct consolidation loans require students to pay off their loans for 10 to 30 years. The repayment length will vary based on what one owes, with payment periods lasting longer if more student loan debt is involved. As a result, a loan with a total amount of $30,000 can take about 20 years to pay off, while anything worth over $60,000 will take 30 years to cover.

Emily P. had to take out about $60,000 of money during her four years of study at a public university in Minnesota. While tuition cost about $10,000 per year, the cost of room and board and other items was high.

But Emily was able to cover the $60,000 that she borrowed over the course of about ten years. "I was able to find a great job after I graduated, and I used the money I was earning from that job to help me complete my monthly payments over ten years," she said.

"I had to manage some of my funds in the years after graduating, though," she added. "I was able to get some support from my family in finding a place to live near my worksite, and there were a few times where I could complete more than just the monthly minimum payment."

But Emily didn’t have it easy all the way through, as she had to strike a deal with her parents to afford an apartment for a few years, helping her reduce her monthly expenses. She knew she had to find people she could trust to help her keep her expenses under control after graduating, and she had some people who were ready to help.

Emily was positive about her experience in managing her student loan debts, but she could also be one of the lucky ones who could handle them well. College expenses are increasing, and many struggle to pay off their debts. These expenses make it harder for people to manage their lives, although measures are available to keep those debts in check.

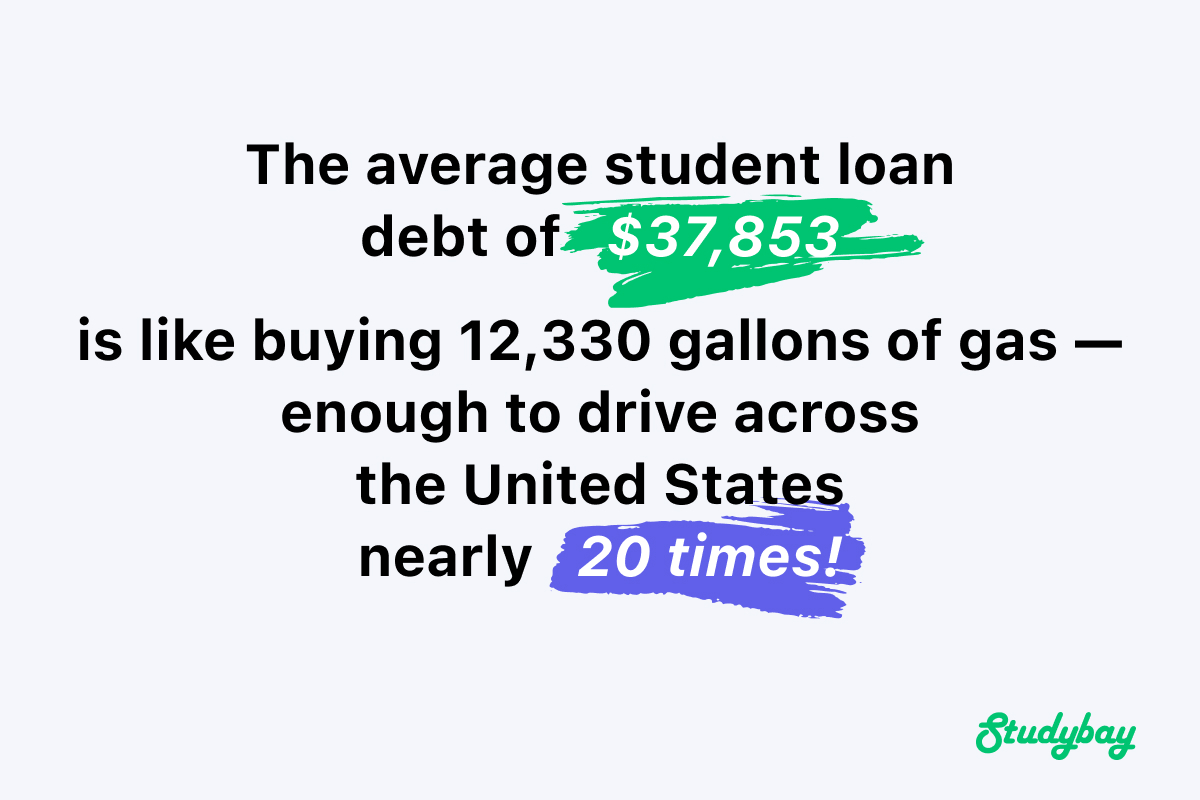

To put this into perspective, considering the average student loan debt of approximately $37,853 per borrower and the national average gasoline price of $3.07 per gallon, this debt equates to roughly 12,330 gallons of fuel—enough to drive across the United States nearly 20 times.

The Total Keeps Rising

The worst part about paying off these loans well after college is that their total costs often end up being greater than whatever someone paid at the start.

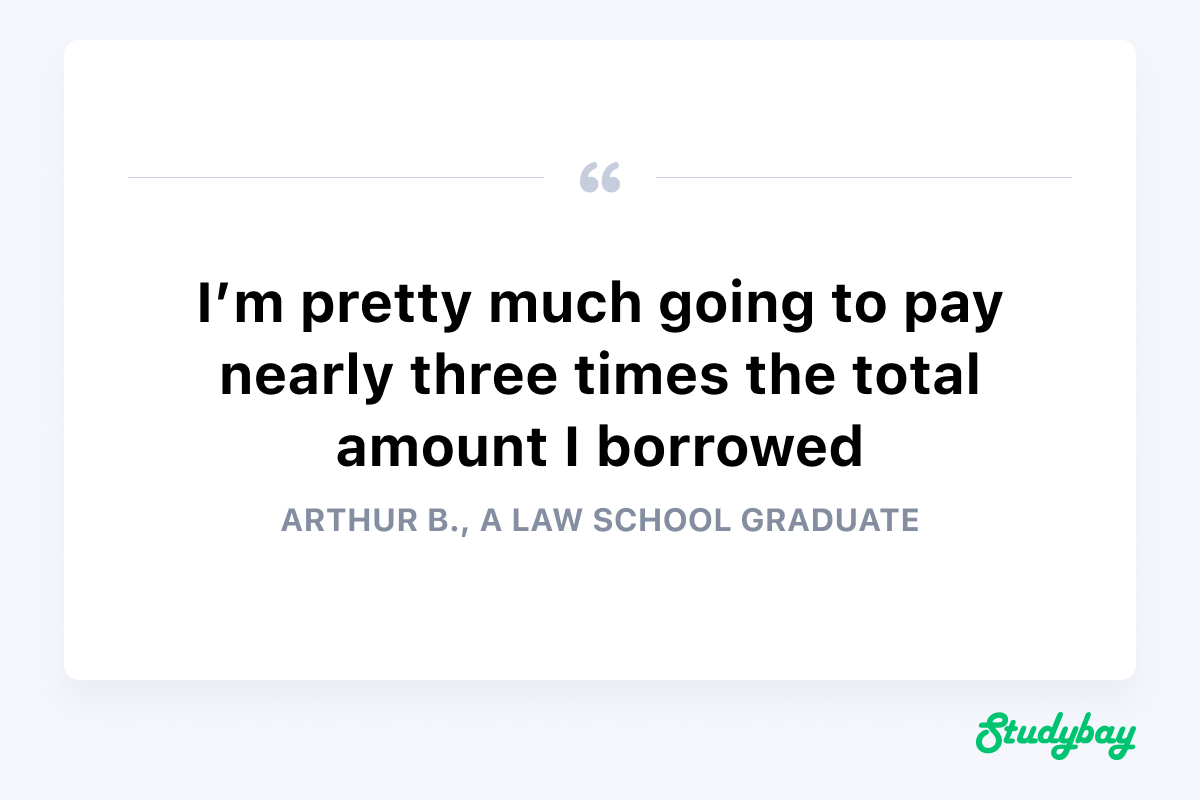

One person who has been struggling with his loans is Arthur B., who borrowed $120,000 on a 30-year loan to pay for his law school expenses. Arthur was hoping that the loan could be paid off through his future job in the law field.

While Arthur has managed to make his way through the industry to where he’s now part of a dedicated law firm, the debt he’s been dealing with has been extreme.

"My loan had an interest rate of 7.5 percent," Arthur says. "And I’m making at least $800 in monthly payments. But the way interest is adding up, it’s getting to where it will take more than thirty years for me to pay it off. It’s hard to manage that expense alongside so many others I’ve incurred."

"I’m pretty much going to pay nearly three times the total amount I borrowed," he also says. "I keep making extra payments here and there, and it’s still not doing much. I’m still probably going to spend at least $300,000 on my loan."

This situation has hurt Arthur, as he has been stuck renting an apartment instead of acquiring his own home with a separate mortgage loan. He’s also had to cut back on many other things in his life, including visits with his extended family.

"If I had to tell people who want to get student loans anything, it’s to consider not borrowing so much," Arthur says. "If I hadn’t borrowed as much, I wouldn’t be in anywhere as much of a hole as I am now."

Different Repayments Based on Different Situations

Age Group

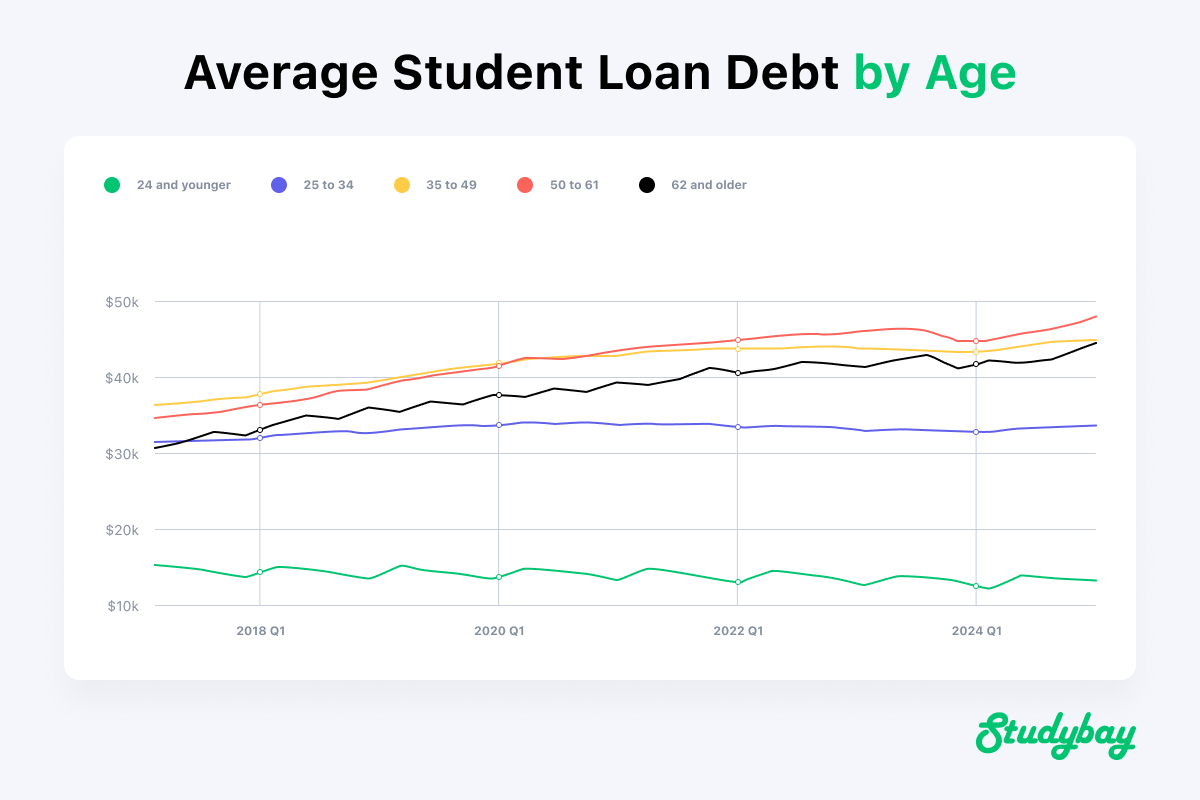

The student loan debts alumni hold vary through many situations. A The Motley Fool report from 2024 states that older alumni tend to owe more on their loans than others.

The Motley Fool report says that during the fourth quarter of 2024, the average person 24 or younger owed about $14,000 in debt. For those 25 to 34, that number rises to $33,000. People in the 50 to 61 range have the most debt, as they average about $47,000 in debt.

These numbers are influenced mainly by how older persons are more likely to have gone through postgraduate education programs that come at an additional cost. Therefore, they are spending extra in the hopes they can attain higher positions with their more advanced degrees. But in the process of doing so, those people are risking the potential of not finding anything that offers a high enough salary to pay for the expenses.

Income Levels

The total amount of student loan debt is typically higher among those who earn more money, but much of this comes from those students paying more to attain postgraduate degrees. A 2024 analysis found that People from the 0 to 50 percentile, or those in the bottom half of income levels, tend to have less than $10,000 in student loan debt on average, or less than $15,000 for the age 25-40 households.

The totals continue to rise as a person earns more money, with those in the 80th to 90th percentile owing about $20,000 on average. That total rises to $46,000 for the age 25-40 households.

Those numbers eventually drop as people reach the top 10 percent of income earners. An age 25-40 household will owe around $30,000 in debt from the 90th to 95th percentile, while that total drops to $25,000 from the 95th to 99th percentile.

The amount a person earns based on percentile can dramatically vary. Whereas someone at the 50th percentile will earn about $50,000 a year, someone at the 80th percentile gets $100,000.

A person who earns more income should be capable of paying off student loans. But with the cost to get a degree that helps someone find jobs that pay enough being so high, those student loan costs continue to be exorbitant.

Degree Type

The total amount of student debt one owes based on degree type is another concern that could prevent students from wanting to attain further degrees. For example, a person earning a bachelor’s degree might not want to pursue a master’s degree due to the added debt involved.

The earlier discussion of Arthur spending more on his loans is an example of this point. Arthur had to spend more than others to attend law school, what with that type of school having higher standards.

The fintech company SoFi reports that in 2025, people who seek master’s or doctoral degrees tend to spend more on student debt than those who get bachelor’s degrees. For example, a person with a Master of Business Administration or MBA degree will owe about $80,000 in student loan debt on average. This total is compared with the average salary of $120,000 an MBA holder has. Meanwhile, an average lawyer with an advanced law school degree will have about $130,000 in debt on average, which is close to the average salary of $145,000 someone in that position would hold.

A Look at the Economic Impact

Handling Investments

The economic impact of student loan debt is making it harder for students to manage various investments. In addition to spending more on their loan payments, they’re also not looking for new homes.

The National Association of Realtors writes that in January 2025, the homeownership rate for people under 35 has reached a new low. The organization has long listed first-time homeowners from 28 to 33 years of age. But whereas about 44 percent of home buyers in 1981 were first-time buyers, that number dropped to 24 percent in 2024. Meanwhile, fewer than 40 percent of homeowners are under the age of 35.

The organization also reports that in 2024, the median age of first-time buyers was 38, while the median age for repeat buyers was 61. This 23-year gap is a massive jump from 1981, when the numbers for first-time and repeat buyers were 29 and 36 for a seven-year divide.

Planning For Retirement

The student debts people are acquiring have also made it tougher for them to save for retirement. For example, people aren’t as likely to make 401(k) contributions to help increase their retirement savings because they’ve got other financial obligations to bear.

Empower lists that a person in one’s twenties will have a median 401(k) of around $35,000. That number goes up to over $70,000 in one’s thirties and over $150,000 in the forties. The amounts someone can get in this retirement fund can be significant, especially since many businesses will match employee contributions. But people aren’t so willing to make contributions when they’re younger because they need funds to pay for college debts.

It’s also harder for people with student debt to make contributions to individual retirement accounts, or IRAs. Whereas an IRA can dramatically rise in value based on how much one makes in contributions, it’s tough for new graduates to make contributions to help get a good start on their IRAs.

Fidelity writes that people can make annual contributions of up to $7,000 on their IRAs, but those over 50 can make $8,000 contributions. But despite this opportunity, people under the age of 30 have minimal IRAs with less than $10,000 in them.

If those people with less than $10,000 in an IRA kept making maximum contributions for at least five years, their IRAs could be worth at least $50,000. By contributing for another five after that, the total can rise to over $200,000 if one’s assets are managed well.

The Government’s Expenses

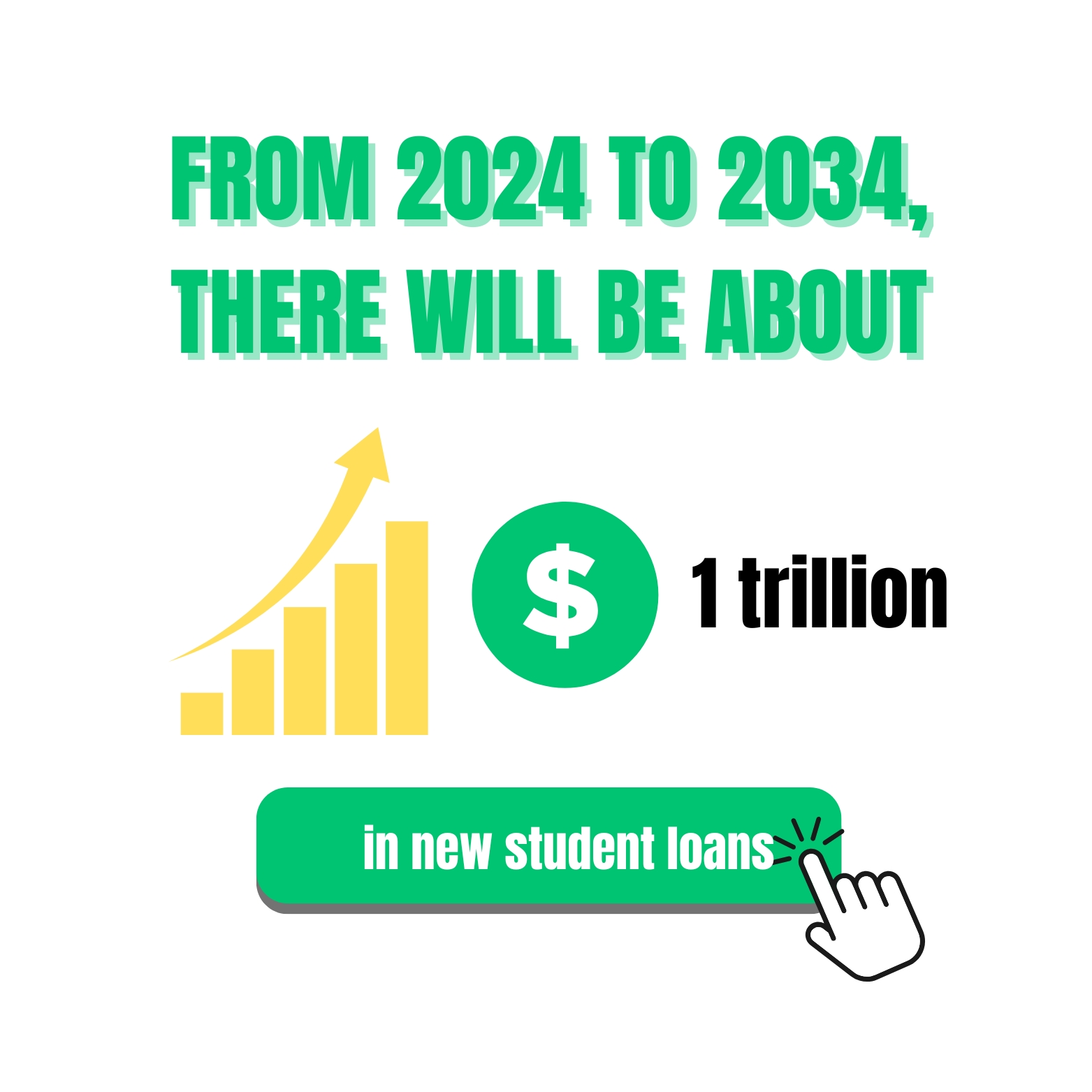

Student loan totals are expected to rise in the future, and with this comes a potential for the federal government to lose money. The Cato Institute reports that from 2024 to 2034, there will be about $1 trillion in new student loans. The institute also argues that the federal government would lose 19 cents for each dollar students borrow as it becomes more difficult for alumni to pay off their loans.

Federal government loan programs had long been considered profitable for the government, as simple loans could be offered with the government taking in profits from the interest payments students make. But as these loans become more difficult for students to pay off, the government will potentially lose money from these investments.

Possible Reforms

As difficult as these student loan debts can be for so many people, some reforms could go into place to help students afford their loan costs. Income-driven repayment plans are worth noting, as these plans involve establishing a targeted repayment plan where a borrower pays an amount each month proportional to whatever income one earns during that time.

Another solution for reform is to establish a setup where a person can cut one’s monthly payments in half and be forgiven from the rest of the debt if that someone makes regular payments for ten to twenty years. This measure would help people pay off at least 70 cents of every dollar they borrow, although there is some reluctance to adopt a reform like this one. It’s possible someone might still pay less than 70 cents per dollar.

Other Programs to Manage Expenses

It’s also possible that people can use deferred payments to help them handle their loan debts. A deferment plan allows a person to suspend payments for a brief period, but interest will still build on the loan during that deferment period. This plan can work for people who are looking for employment to improve how well they can complete their regular payments.

Plans for student loan forgiveness may also be available to people who qualify. Teachers, government employees, and nonprofit agency workers are among those who qualify to reduce some or even all of their expenses.

A good story about this issue comes from Charles S., who took a teaching position at a secondary school after graduating with a degree in education. He had about $40,000 in student loan costs after graduation, but he qualified for a forgiveness plan that covered nearly half that cost.

"To qualify for this forgiveness plan, I had to work for five consecutive years at a school that qualified," Charles said. "My school qualified for the plan based on its status and the clientele. So with that, I could not only pay off much of my loan but also get the government to cover a sizeable amount for me."

"Everything added up well, and I didn’t have to spend as much as I worried I’d have to," Charles adds.

Final Say

The struggles of trying to pay off student loan debts are daunting. The expenses can be very high, and it often becomes tough to pay off a loan before interest starts adding up. It’s also harder for students to make the necessary investments for their lives and retirements because they don’t have as much money to spend on those things.

But with the right plans for living and various reforms, it may be easier for people to pay off their debts. It takes work and effort, but finding plans for managing those debts can work well.